- Bits + Bips

- Posts

- Stablecoin Blockchains Are Coming. Here's Why These Two Giants Should Be Nervous

Stablecoin Blockchains Are Coming. Here's Why These Two Giants Should Be Nervous

Issuers are riding shotgun alongside L1s. Now they want to drive.

Stablecoins grew out of crypto’s — and in particular Bitcoin’s — inability to maintain any sort of price stability. For years they have been welcomed by L1s that adopted them as the lifeblood that makes their blockchains go.

But now, stablecoins have regulatory blessing from Washington, D.C., and L1 blockchains do not. And they no longer seem content to be an add-on to blockchains still searching for product-market fit.

Today’s newsletter is brought to you by Mantle

Mantle is building the Blockchain for Banking — where TradFi meets Web3. Explore real-world financial tools, powered fully on-chain.

Stablecoin Blockchains Are Coming. Here's Why These Two Giants Should Be Nervous

With the GENIUS Act passed, stablecoins are set to surge — and major issuers now aim to run their own layer 1 blockchains, not just build on others. If they win, someone has to lose.

Stablechains are coming. Who should be most worried? (ChatGPT)

Although stablecoins were never supposed to exist when Bitcoin was created more than 15 years ago, they turned out to be a godsend for the industry. It did not take long for many to realize that bitcoin, and other assets like ethereum, solana, XRP, etc., could not serve as substitutes for the U.S. dollar because they were too volatile.

Stablecoins were the perfect solution. They ran on public blockchain rails but maintained price parity with a given peg — often the dollar. Their market cap grew from under $1 million in 2017 to $271 billion today as they expanded across blockchains, primarily Ethereum and Tron, and became the primary liquidity engine for spot trading, DeFi markets, and payments. By far the two largest stablecoins are Tether (USDT) and USD Coin (USDC), with respective market capitalizations of $164.85 billion and $65.22 billion.

But those issuers no longer seem content to just ride the rails of other blockchains. They want to be the engine that makes blockchain payments go. The team behind Tether has invested in multiple stablecoin-focused blockchains (Plasma and Stable) and payments giant Stripe appears to be working on its own blockchain. Then, on Tuesday, Circle Financial (CRCL), the primary issuer behind USDC, announced plans for Arc — its own L1 blockchain customized for payments.

Buttressed by the July 2025 passage of the GENIUS Act, stablecoins are set to explode. Right now their $271 billion supply only represents about 1.2% of the total M2 money supply of $22.02 trillion. Treasury Secretary Scott Bessent says that stablecoins could grow to $3.7 trillion by the end of the decade, if the infrastructure gets built.

(The Block)

Circle CEO Jeremy Allaire was quite frank in saying that the current mix of blockchains is insufficient to meet the needs of a modern payments system.

“We are at the fulcrum of a massive mainstream embrace of stablecoins in the financial system, and firms are racing to build on this infrastructure,” said Allaire. “But until now, the blockchain infrastructure needed to meet the most intense demands of major financial firms and enterprises has simply not existed.”

But for Arc or any of these other blockchains to succeed, they will need to take market share from someone. Here’s why there is an opportunity and who could be vulnerable.

Where Today’s Blockchains Fall Short

Ethereum

Pick a major blockchain, and you will find something that can be improved when it comes to stablecoins and payments.

Ethereum, by far the biggest blockchain outside of Bitcoin with a market capitalization of $563.7 billion, is too slow and expensive for widespread payments use. Its current average transaction fee is $1.05, according to Token Terminal (see below). While that may seem competitive with card networks and their interchange fees, there are a couple of things to keep in mind. First, the Ethereum network can only handle about 20 transactions per second, and these fees can wildly move up or down during times of peak use. It is also important to note that these transaction fees must be paid in ETH, meaning that users have to keep a reserve on hand whose value can fluctuate based on market dynamics.

(Token Terminal)

The fees averaged a shade under $20 per transaction for the first half of 2021 and peaked above $50 that May. No high-volume, low-value payments business will accept that level of variance.

This shortcoming does not mean that Ethereum does not have a sizable role to play in payments, but it will likely focus on the high-value, low-volume side of the spectrum. “Ethereum is the leading chain in terms of total value locked and economic security, and that makes it the natural platform for institutional finance,” said Zach Pandl, head of research at Grayscale Investments in a February interview.

Base

These issues with Ethereum are not new, and that is why many industry analysts look to L2 blockchains, such as Base, as a way to get the best of both worlds. In this case that means the speed and low cost of a card network with the economic security of Ethereum. Coinbase and Circle are actually close partners and are working to promote USDC adoption on Base.

Transactions on Base typically cost a fraction of a cent. But many of these networks, including Base, also remain experimental. While this network has seen dramatic growth in terms of developers and market attention, it remains highly centralized because Coinbase is the only sequencer operator on the network. For L2 blockchains, sequencers fulfill a similar function as L1 validators or miners.

This vulnerability became apparent in early August when Base went down for 33 minutes due to an issue with its sequencer. If other sequencers had been available, the network may have been able to continue operating in the same way that Bitcoin or Ethereum doesn’t go down if a major miner or staker gets taken offline.

(Dune Analytics)

Tron

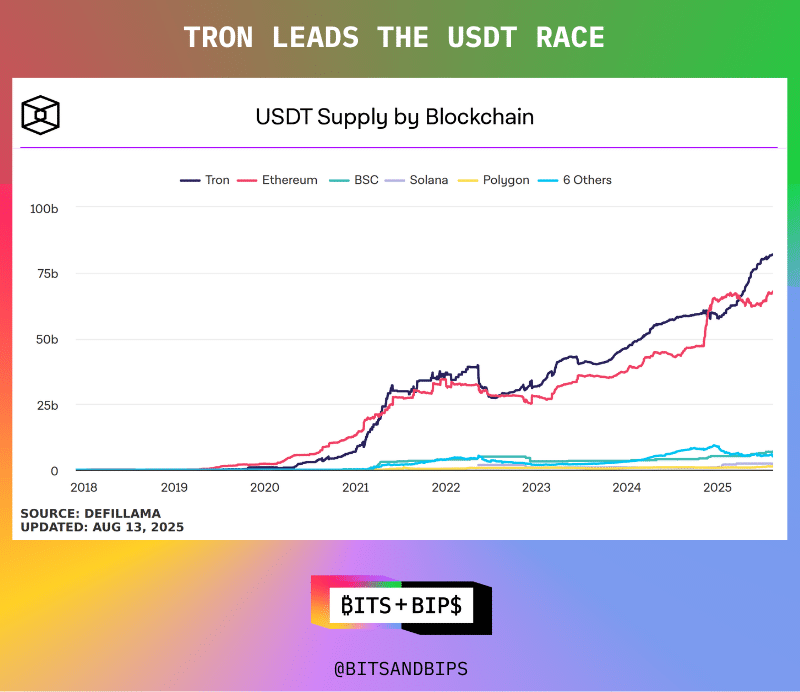

And finally, it is worth discussing Tron, the $36.2 billion blockchain launched by Chinese billionaire Justin Sun. Although Ethereum tends to have higher mindshare, especially in the Western world, Tron is the dominant chain when it comes to USDT, hosting $81.89 billion of the asset.

And it has long had a reputation for being a low-cost blockchain, which matters especially for users in emerging markets. “You’re talking about some of the most cost-sensitive markets on Earth,” Chris Maurice, chief executive officer of African-focused crypto exchange YellowCard, said to Forbes when I profiled Justin Sun in March. “In some of these countries people will spend eight hours of their day to save a couple of bucks, and $50 versus a few cents is a pretty tremendous difference.”

(The Block)

But Tron is not as cheap as many people think. Its average transaction costs $1.70, which is higher than Ethereum’s.

(Token Terminal)

Additionally, Tron actually charges orders of magnitude more for transactions that involve USDT than for simply sending its native TRX token. It only costs about 39 cents to send TRX over the network, but a USDT transaction costs an average of $4.83.

Maybe it is for this reason that Maurice sees stablechains like Arc as a potential competitor to Tron in particular. “I think that these players have a lot of capital available to push their chains and infrastructure and they are looking to control the rails rather than just the tokens,” said Maurice. “I think it's a brilliant move and they have the resources to be successful, which makes them a big threat to Tron.”

Representatives of Tron and Justin Sun did not respond to requests for comment before publication of this story.

Visa, the Blue and White Whale

Given the limitations of existing blockchains when it comes to payments, it stands to reason that these new stablechains will try to take some market share even while the operators all play nice in public. “[These new blockchains] are competing with existing L1s, that’s for sure,” said one industry analyst who requested anonymity.

But the main target is going to be the real industry incumbents like the card networks. “Visa moves somewhat north of $10 trillion a year through its consumer to business and business to business rails,” said Circle Chief Financial Officer Jeremy Fox-Geen in Tuesday’s earnings call. The industry analyst quoted above said that “if [Circle] can take 10% of Visa’s volume, that would be massive.” He also pointed out how JPMorgan “moves somewhat north of $10 trillion a day in gross money movement and gross money settlement as well as other use cases.”

And it appears that Circle is using a dual strategy to either cooperate or compete with Visa, depending on how you look at it. On the one hand, the company is letting clients settle transactions in USDC. According to one company report, as of April 30, 2025, the company had settled $225 million in USDC transactions.

Visa did not respond to request for comment prior to publication.

But obviously that is a drop in the bucket in terms of Visa’s overall volume and will not do much to move the needle in terms of Circle’s bottom line, which is far too concentrated in reserve income. According to its Q2 earnings, its reserve income, which consists of the money earned by investing USDC collateral in cash-like instruments, was $634 million. But it only made $24 million from its subscription and services business, which includes fees from processing USDC transactions and moving tokens across networks.

Moving forward, the company wants those line items to be in balance. This shift could be increasingly critical once President Trump replaces Fed Chairman Jerome Powell with a friendly successor who could try to lower the federal funds rate. Circle’s reserve return rate in Q2 was 4.1%, and Trump is musing about a 300 bps reduction in the future.

And it appears that Circle is going to bet its chips on Arc, a blockchain designed to be the baselayer for payments.

“Financial institutions and regulators expect deterministic finality, which Arc will achieve with Circle vetted professional validators and its novel consensus mechanism,” said Allaire. “Arc will also offer configurable privacy controls with opt-in confidential transfer features, which is essential for real world business and financial applications, and also supports regulatory compliance.”

And nobody is going to have to pay transaction fees in a volatile L1 token.

Related content:

Reply